The Goods and Services Tax (GST) is a tax on goods and services consumed in India. GST is an indirect tax that has replaced many other indirect taxes in India, such as excise duty, VAT, and services tax. GST has been in force since 1st July 2017 based on the Goods and Service Tax Act passed by the Indian Parliament on March 29, 2017.

A ‘taxable person’ under the GST Act is someone who conducts business in India and is registered or needs to be registered under the GST Act. A taxable person can be an individual, HUF, company, firm, LLP, an AOP/ BOI, any corporation or Government company, body corporate incorporated under the laws of a foreign country, cooperative societies, local authorities, governments, trusts, or artificial juridical persons.

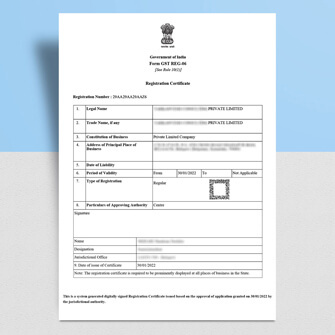

GST registration can be obtained voluntarily by any person or entity irrespective of turnover. GST registration becomes mandatory if a person or entity sells goods or services beyond a certain turnover.

Service Providers: Any person or entity who provides service of more than Rs.20 lakhs in aggregate turnover in a year is required to obtain GST registration. In special category states, the GST turnover limit for service providers has been fixed at Rs.10 lakhs.

Goods Suppliers: As per notification No.10/2019 any person who is engaged in the exclusive supply of goods whose aggregate turnover crosses Rs.40 lakhs in a year is required to obtain GST registration. To be eligible for the Rs.40 lakhs turnover limit, the supplier must satisfy the following conditions:

If the above conditions are not met, the supplier of goods would be required to obtain GST registration when the turnover crosses Rs.20 lakhs and Rs.10 lakhs in special category states.

Special Category States: Under GST, the following are listed as special category states – Arunachal Pradesh, Assam, Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh, and Uttarakhand.

Aggregate Turnover: Aggregate turnover = (Taxable supplies + Exempt Supplies + Exports + Inter-State Supplies) – (Taxes + Value of Inward Supplies + Value of Supplies Taxable under Reverse Charge + Value of Non-Taxable Supplies).

Aggregate turnover is calculated based on the PAN. Hence, even if one person has multiple places of business, it must be summed to arrive at the aggregate turnover.

There are various types of GST registration: regular, casual taxable persons, non-resident taxable persons, and eCommerce operators. Casual taxable persons, non-resident taxable persons, and eCommerce operators are required to obtain GST registration irrespective of turnover limit.

Casual Taxable Persons: The GST Act defines a casual taxable person as a person who occasionally supplies goods or services in a State or a Union territory where the entity has no fixed place of business. Hence, persons running temporary businesses in fairs or exhibitions or seasonal businesses would fall under casual taxable persons under GST.

Non-resident Taxable Persons: Non-resident taxable person (NRI) under GST is any person or business or not-for-profit supplying goods or services but has no fixed place of business or residence in India. Thus, any foreign person or foreign business or organization supplying goods or services to India would be a non-resident taxable person – requiring compliance with all GST regulations in India.

E-Commerce Operators: Electronic commerce operator is every person who owns, operates, or manages a digital or electronic facility or platform for electronic commerce. Thus, any person selling through the internet can be termed as an eCommerce Operator requiring GST registration irrespective of business turnover.

©2022. Trace Quality . All Rights Reserved.